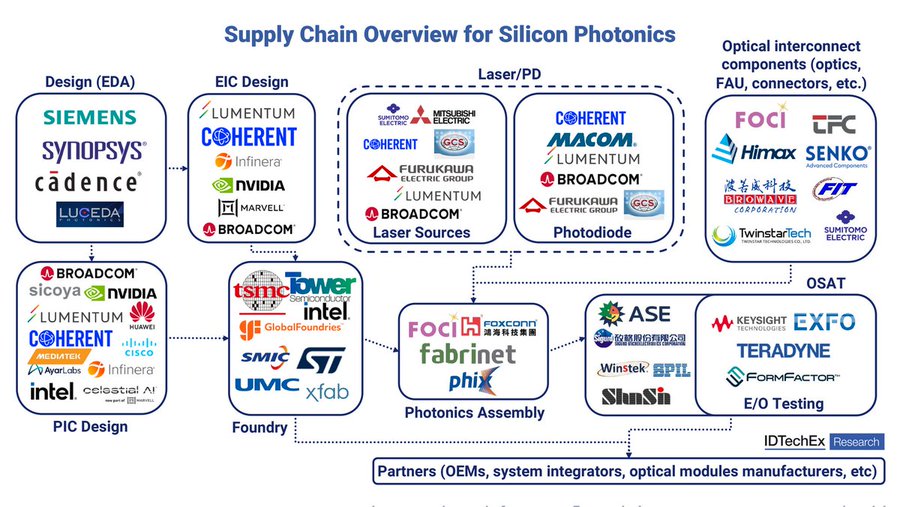

The silicon photonics supply chain diagram is one of the most important investment maps in technology right now (Save this).

Every AI data center being built depends on what's in that chart and the companies inside it are just starting to show what the revenue ramp looks like.

Here are the 10 stocks I am watching.

1. Broadcom (AVGO): Broadcom's AI revenue rocketed 106% to $8.4 billion in its most recent quarter, driven by custom accelerator chips for Google, Meta, and Anthropic, plus AI networking silicon. It is one of the few companies doing both the switch silicon and the photonics integration needed for co-packaged optics at hyperscale. The silicon photonics diagram shows Broadcom appearing across multiple layers, PIC design, laser sources, photodiode, and EIC design.

2. MACOM Technology (MTSI): MACOM is quietly positioning itself at the inflection point of the 1.6T and 3.2T optical transceiver transition. In March 2026 it launched 448G PAM4 modulator drivers among the first in the industry and joined Broadcom, Cisco, and Semtech in the 400G Optical MSA standards consortium. In June 2026 it introduced hot via chip scale technology, eliminating wire bonds in its AlGaAs packaging.

3. Marvell Technology (MRVL): Marvell is the DSP engine inside many of the optical modules in that chart. Its custom AI silicon, built for hyperscalers who want to own their accelerator architecture is the fastest growing part of its business. It sits at the EIC design layer and supplies the digital signal processing that makes high-speed optical links work reliably at scale. As the industry shifts from 400G to 800G and 1.6T, every step requires more sophisticated DSPs and Marvell captures more revenue per module shipped.

4. Keysight Technologies (KEYS): Every optical module that ships from every fab in that chart has to be tested before it reaches a data center. Keysight is the global leader in electronic and photonic test equipment. As optical speeds push to 800G and beyond, the testing instrumentation has to keep pace and it commands premium pricing.

5. FormFactor (FORM): FormFactor is the most underappreciated name in this entire chart. Q1 2026 revenue was $226 million, up 32% year over year, beating estimates with non-GAAP EPS of $0.56 versus $0.44 expected. It acquired Keystone Photonics in December 2025, becoming the leading wafer-level silicon photonics test platform for co-packaged optics production. Its partnership with Advantest created the world's fastest automated photonic alignment test system with nine-axis nano-precision. Over 100 of the world's leading silicon photonics manufacturers use FormFactor systems meaning every CPO chip that ships from any fab in that diagram gets tested on FormFactor equipment.

6. Teradyne (TER): Teradyne sits in the E/O Testing layer alongside Keysight and FormFactor. As silicon photonics chips get more complex, integrating lasers, modulators, photodetectors and electronic drivers on a single chip, the test complexity explodes. Teradyne's automated test equipment platforms are expanding from traditional semiconductor testing into photonic integrated circuit validation. It also has a robotics division, which ties the silicon photonics thesis directly back to the humanoid supply chain story.

7. EXFO (EXFO): EXFO is a fiber optic and network testing specialist that has been building testing platforms specifically for coherent optical and silicon photonics applications. It sits directly in the E/O Testing box of the supply chain map. It's a smaller cap, which means the upside from the optical buildout is amplified relative to its size. It is one of the few companies that tests live network optical performance meaning it gets pulled in not just at the component manufacturing stage but every time a data center expands or upgrades.

8. Foxconn Industrial Internet (FXCOF): Foxconn appears twice in that supply chain diagram in both Photonics Assembly and Optical Interconnect and that is before you even consider its server business. Q1 2026 revenue hit $66.6 billion, up 29.7% year over year, with AI servers now representing more than 50% of total server revenue. Its silicon photonics CPO switches entered mass production in Q3 2026 with full year shipments forecast at 10,000 units. It is boosting capex 30% specifically for AI infrastructure. Almost no retail investors think of Foxconn as a silicon photonics play and that's the opportunity.

9. Sumitomo Electric (SMTOY): Sumitomo appears in two places on that supply chain diagram as an optical interconnect component supplier and in the laser/photodiode layer. The company has been a foundational supplier to the fiber optic industry for decades and is now scaling its silicon photonics packaging and optical connectivity capabilities for AI data center applications.

10. Synopsys (SNPS): Every silicon photonics chip has to be designed before it can be manufactured. Synopsys is the dominant EDA software company for photonic integrated circuit design and sits at the very top left of that supply chain map. The shift toward co-packaged optics means optical and electronic chip design have to be co-simulated, exactly the kind of complex, multi physics workflow Synopsys is built for. Its photonics design tools are already embedded across every major chip company in that diagram. The more complex the chip, the more customers pay for Synopsys tools.

Milk Road Pro is tracking every layer of the silicon photonics supply chain, from Broadcom and Marvell to the testing names most investors still don’t know.

Join Milk Road Pro for the full breakdown and for all our AI trades for just $1 using the link below!