Pinned Post

Legendary investor Gavin Baker: “If you look at the valuations for all these AI names, they can’t all be accurate.”

Here is the problem:

Memory stocks are trading at 3 to 5 times earnings. NVIDIA is trading at what he describes as a really low PE. Some other accelerator companies are at reasonable multiples.

And then on the other side of the AI infrastructure stack, power, cooling and optical names are trading at multiples that imply a very different future.

Those two sets of valuations are internally contradictory.

If the power, cooling and optical names are right, then NVIDIA and memory are dramatically underpriced and are going up a lot from here. If NVIDIA and memory are correctly valued, then everything else in the stack is overpriced and is probably going to underperform from here.

The key is figuring out the correct side of the trade.

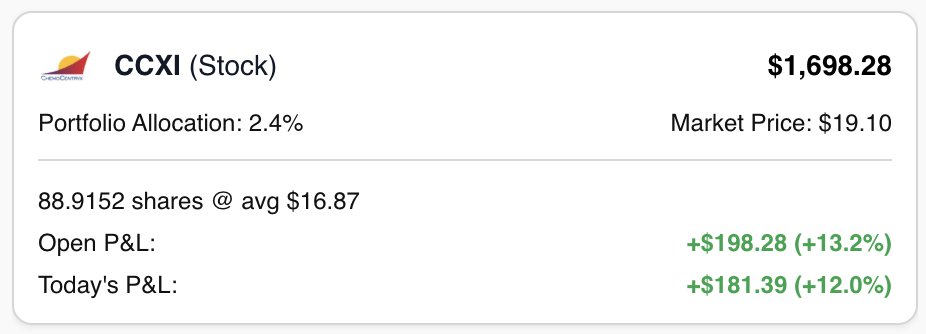

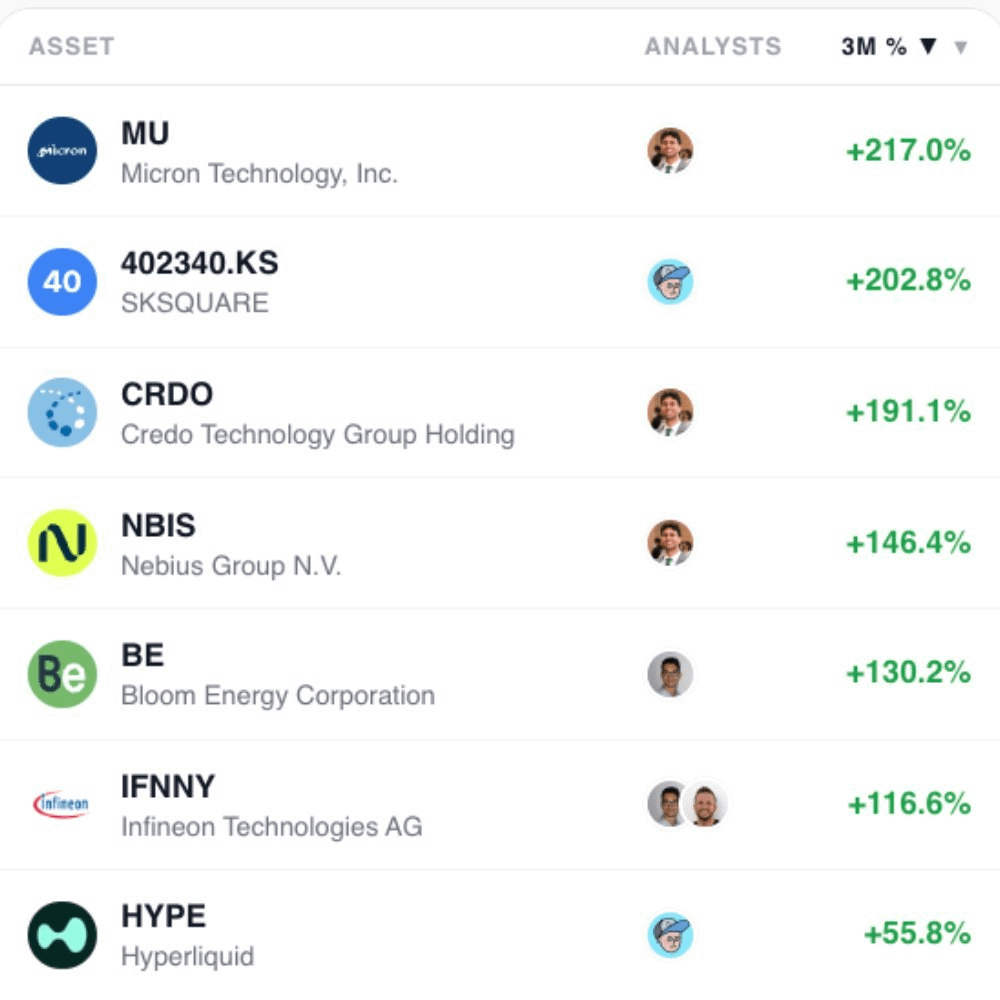

Our analysts at Milk Road PRO have taken positions in various AI names based on this thesis. They were very early to $MU, $NBIS and $CRDO with over 100% gains.

Get access to their exact portfolios for $1 (link in bio).

Gavin Baker says DRAM and HBM DRAM is the single most important bottleneck in all of AI (Save this).

All the stocks that supply it are still trading at a discount to everything else in the stack.

His argument is foundational:

Model performance is constrained by how much memory is available and how fast it can move data. That is why Elon Musk is specifically targeting memory in his tariff strategy.

The supply side makes this more interesting.

For the HBM DRAM that AI servers actually need, there are only three companies in the world that can manufacture it: Micron, SK Hynix and Samsung.

Micron's most recent quarter added another layer: they announced supply chain agreements covering roughly 50% of their revenue with just four customers. The floor pricing in those contracts is already above prior cycle peak gross margins.

Every other part of the semiconductor supply chain, equipment, wafer fab, the rest of the stack, has already re-rated to premium multiples. DRAM stocks are still cross-sectionally cheap.

Our analysts at Milk Road PRO have been very early to the memory trade with SK Hynix and Micron.

Get access to their exact portfolios for $1. (link in bio)

6

20

147

75,129