Pinned Post

The three biggest memory companies on earth just told you exactly when supply gets better and the answer is not anytime soon (Save this).

The AI stack has three layers, chips at the bottom, models in the middle, applications at the top and memory sits at the foundation of all of it.

The problem is the foundation cannot keep up with what is being built on top of it.

Every AI chip, Nvidia H100, H200, B200 requires High Bandwidth Memory (HBM) stacked directly on it and HBM takes roughly 3x the wafer capacity of standard DRAM to produce.

The result is demand is already far outstripping supply.

Micron's entire 2026 HBM output is fully pre-sold and allocated to hyperscalers and new orders are being deferred to late 2027, key customers are currently receiving only 50–67% of their demanded HBM volume.

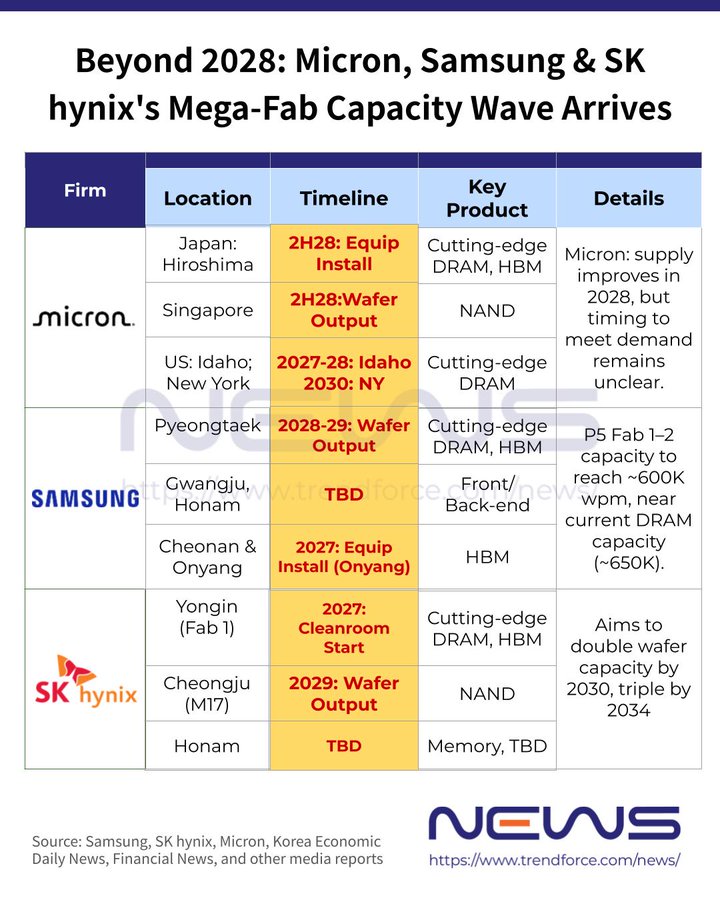

The chart maps out when new fab capacity comes online and the insight is that none of it matters yet.

All the new fabs listed, Micron's Hiroshima, Samsung's Pyeongtaek P5, SK Hynix's Yongin are either still being equipped or won't produce a single wafer until 2027–2029 at the earliest.

Until then, all three companies are running on fixed, cannot be expanded capacity.

Micron has three expansion waves, Hiroshima equipment install happening now in 2H 2028 for cutting edge DRAM and HBM, Singapore wafer output 2H 2028 for NAND, Idaho meaningful volume mid-2027, New York not until 2030.

Samsung's Pyeongtaek P5 full wafer output for cutting edge DRAM and HBM does not arrive until 2028–2029, Onyang gets HBM equipment installed in 2027, Gwangju/Honam has no confirmed timeline at all.

SK Hynix's Yongin Fab 1 only starts cleanroom construction in 2027, Cheongju M17 NAND output in 2029 and the company aims to double capacity by 2030 and triple by 2034, meaning real relief is nearly a decade away.

Now here is what the chart does not show.

Even when these fabs open, supply does not catch up to demand because HBM requires precision stacking tools with 12-month lead times and even when wafers are ready, they cannot be assembled into usable HBM fast enough.

The supply will be tight for many years to come, long Micron and make sure to follow me @melvininvests for more updates around Memory and Semi's.

7

17

64

7,788