I recently read SVRC Research’s April 2026 “State of Robotics” report, and it reinforced many of the long-term themes I’ve been following in humanoid robotics and embodied AI.

The report identifies several companies leading the U.S. robotics race, including Figure AI, Agility Robotics

$CCXI , Apptronik, Tesla, Boston Dynamics, Physical Intelligence

$PI , 1X Technologies, Amazon Robotics, Covariant, and Skild AI.

One of the biggest takeaways is that the U.S. remains the global leader in AI models, robot intelligence, embodied AI, and autonomous driving software. The next generation of robots won’t simply follow pre-programmed instructions—they’ll be able to understand, learn, and adapt to real-world environments using foundation models.

That said, China still has meaningful advantages in manufacturing scale, supply chains, and cost-efficient production. Winning the robotics race will require more than great AI—it will also require the ability to manufacture and deploy millions of robots at commercial scale.

The report also highlights several challenges for the U.S., including dependence on rare earth materials, precision actuators, harmonic drives, reducers, and high-performance motors sourced largely from Asia and Europe. Manufacturing capacity, real-world data collection, and regulation remain additional hurdles before humanoid robots can be deployed at scale.

With so many well-funded startups competing, SVRC expects the industry to begin consolidating, with mergers and acquisitions likely starting in 2027 as larger technology companies seek to strengthen their robotics capabilities.

The first wave of adoption is expected in warehouses, logistics, manufacturing, automotive production, healthcare, retail, and industrial inspection, where labor shortages and repetitive work provide the strongest economic incentives.

While many of today’s humanoid leaders remain private, I believe investors should also pay attention to the companies building the ecosystem around them. Potential beneficiaries include:

•

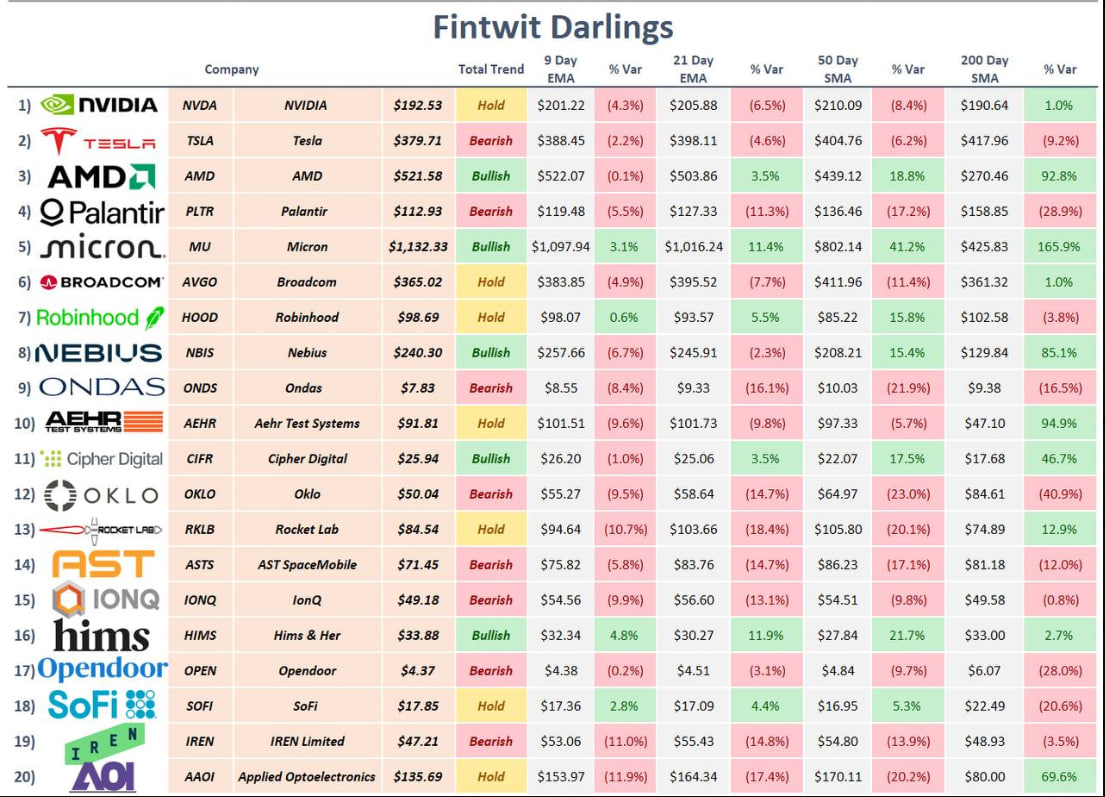

$NVDA – AI chips, robotics software, Isaac platform, and simulation.

•

$TSLA – Optimus humanoid robot and AI.

•

$AMZN – Warehouse automation and robotics deployment.

•

$GOOGL – AI research and robotics through DeepMind.

• Symbotic

$SYM – AI warehouse automation.

• Teradyne

$TER – Owner of Universal Robots and collaborative robotics.

• ABB

$ABB – Industrial robotics and factory automation.

• Rockwell Automation

$ROK – Smart manufacturing and industrial automation.

• Ouster

$OUST – LiDAR sensors for autonomous robots.

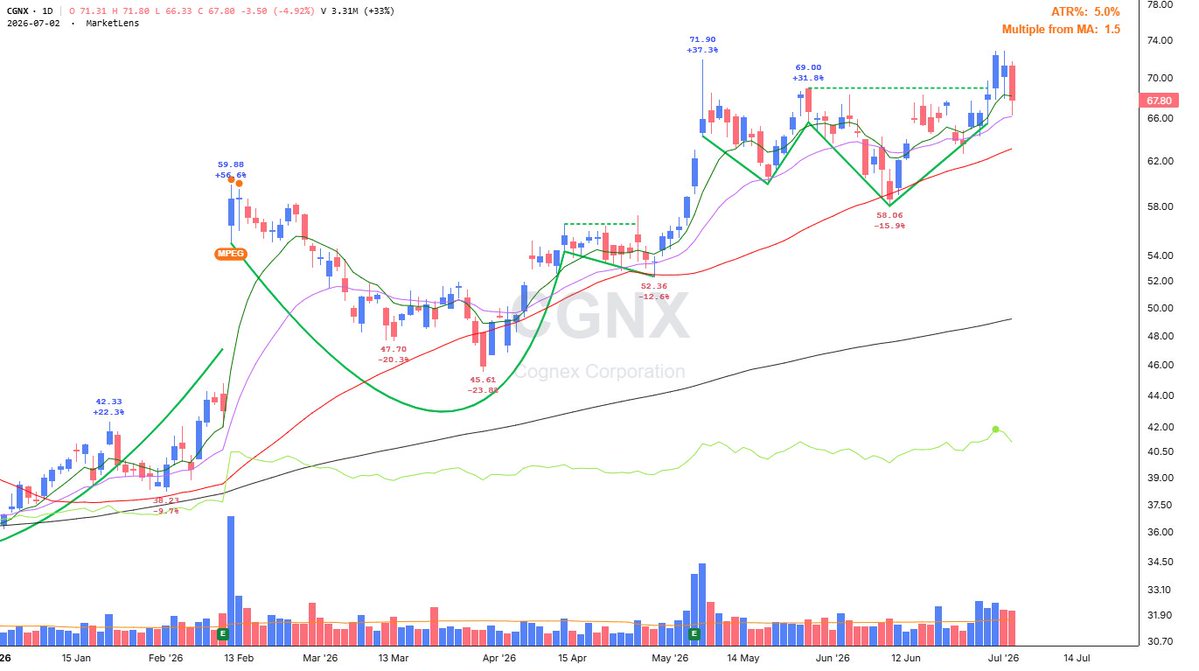

• Cognex

$CGNX – Machine vision systems used in robotics.

• Ambarella

$AMBA – Edge AI processors for robots and autonomous systems.

• Serve Robotics

$SERV – Autonomous delivery robots.

• Micron Technology

$MU)– Memory powering AI inference.

• Corning

$GLW – Advanced materials and optical technologies.

• ON Semiconductor

$ON – Power chips and sensors.

• NXP Semiconductors

$NXPI – Embedded processors and motor control.

• Analog Devices

$ADI – Precision sensing and motion control.

• Texas Instruments

$TXN – Analog chips and embedded processing.

• TE Connectivity

$TEL – Connectors and sensors.

• Aptiv

$APTV – Electrical architecture and autonomous technologies.

•

$HON – Industrial automation and robotics solutions.

On the private side, I’m especially bullish on Figure AI, Agility Robotics, Apptronik, Physical Intelligence, and Skild AI. Meanwhile, China continues to produce strong competitors like Unitree Robotics, UBTech Robotics, AgiBot, and EngineAI.

To me, humanoid robotics is becoming the next major technology platform. Just as AI infrastructure created winners across semiconductors, networking, cloud computing, and power, robotics could unlock opportunities across chips, sensors, batteries, software, machine vision, industrial automation, and advanced manufacturing. This is shaping up to be one of the defining technology races of the next decade.

roboticscenter.ai/state-of-r…