Rather than treating autonomous systems as isolated applications, Konnex is exploring the infrastructure that could allow independent AI agents and robots to interact through transparent rules and shared economic incentives.

That's the perspective that drew me to @konnex_world.

This merch store is so impressive!! Every stadium in the world needs this kind of infrastructure!

the tottenham merch store is so massive and has so much bts merch literally so much more stock than the pop up!

InterLink is redefining Web3 by evolving from community mining into a powerful, operational blockchain infrastructure.#ITLG #ITL #ITLX #InterLink @chakri_prince11 @C_Interlinklabs @kv_interlink @queentanisaX @inter_link @interlinklabsas

Cleo retweeted

Good Afternoon @cityofjohnston

Why do you need contractors hiring H1B Field Engineers for infrastructure projects?

Field Engineer roles are often filled by U.S. workers (civil engineering grads are common in Iowa).

4

99

233

2,944

This is great, but not sure the need to go to Prasenjit house.

BJP need to pay less attention to celebrities and focus on ground level hard working members to achieve Viksit Bharat goal; that is improved infrastructure, good civic sense etc.

2

sholaglorious retweeted

5h

In all the five states in the southeast, Anambra is not among the top three most developed with infrastructure.

So tell me why you want me to vote for your packaged fraud messiah who once had the chance to develop Anambra 🤔

12

8

19

504

bri ✩🐬 IS SEEING BTS AGAIN retweeted

18h

This is why the fossil fuel industry is so desperately fighting renewable energy infrastructure in the US: renewable power works.

France passed a law requiring solar panels on every parking lot larger than 1,500 square meters.

The law took effect in July 2023. Large lots over 10,000 square meters must be 50 percent covered by solar canopies by July 2026. Smaller lots have until 2028.

Exemptions exist for lots with genuine technical or environmental constraints, and for lots already shaded by trees.

France didn't just issue a mandate and walk away. The 2024 Finance Law introduced a Green Industry Tax Credit covering 25 to 40 percent of eligible solar investment costs.

Small businesses largely won't be impacted by the law. It more targets shopping centers, supermarkets, stadiums, and large commercial lots, not Le P'tit Bistrot.

Critics said businesses would just get rid of their parking lots. Carrefour, France's largest supermarket chain, is actually enthusiastically installing solar canopies across 350 stores, covering 180,000 parking spaces. It's expected to generate 450 gigawatt hours of power annually, enough to run the stores themselves, and it's using the canopies as a selling point - shaded parking makes stores more attractive to customers.

The projected energy output is expected to be up to 11 gigawatts, equivalent to roughly 10 nuclear reactors, without using a single additional acre of land.

The US has approximately 800 million parking spaces, most of them uncovered asphalt baking in direct sunlight. Should we do this too?

8

971

9,806

114,100

For decades, the Pagdi System has quietly shaped Mumbai's housing market. Yet, it remains one of the most misunderstood concepts in Indian real estate.

Many believe a Pagdi tenant is an owner. Others assume every Pagdi building is a MHADA cessed building. Both assumptions are incorrect.

The reality is far more fascinating.

The Pagdi system sits at the intersection of law, urban planning, redevelopment economics, housing policy, property rights and Mumbai's extraordinary evolution as a city. It has protected generations of tenants, challenged landlords, influenced redevelopment projects worth thousands of crores, and continues to shape the future of one of the world's most land-constrained cities.

Is the Pagdi System still relevant in today's Mumbai, or is it time for a fundamental transformation?

#Mumbai #PagdiSystem #Redevelopment #RealEstate #UrbanPlanning #Architecture #Housing #DCPR2034 #MHADA #RentControl #CityMaking #Infrastructure #UrbanDevelopment #RealEstateInsights

linkedin.com/pulse/how-one-c…

18s

Memory chips stocks fantabulous rally done.

Apple devices price hike done.

What next?

Telecom tariffs hikes coming soon?

Your monthly data consumption is about to get costlier.

Not only your Apple iPhone, iPad or laptops are getting costly, the fuel that people use to run those devices (data) will also get costly soon.

Why?

While telecom operators aren’t buying high-end AI chips (GPUs) to run cell towers, they are getting hit hard by the collateral damage: severe supply chain inflation on core networking hardware and data center overheads. This directly squeezes their financial margins

Core telecom infrastructure—like Internet Protocol Multi-Protocol Label Switching (IP-MPLS) routers and switches—relies heavily on standard DRAM and NAND flash memory.

Because memory manufacturers are prioritizing high-margin AI chips, the cost of standard memory has soared. This has caused enterprise-grade router prices to spike, directly inflating telecom capital expenditure

Data Center Premium: Telecom companies are rapidly shifting to "virtualized" or cloud-based networks and building out their own edge data centers to handle 5G traffic. They are now competing for the exact same real estate, power grids, and cooling infrastructure as the energy-hungry AI data centers. This has pushed up their operational expenditure

Telecom companies cannot simply absorb these rising infrastructure costs. Their margins are already under pressure due to heavy investments in nationwide 5G deployments. To protect their profitability and make sense on ROI , operators are leaning towards Accelerated Retail Tariff Hikes.

With average monthly data consumption rising sharply (touching over 24 GB per user in markets like India), operators need to aggressively improve their Average Revenue Per User (ARPU) to offset hardware inflation.

Ultimately, while the tech giants dominate the AI spotlight, telecom companies are facing a hidden "AI tax" via inflated hardware supply chains.

To survive this cycle with healthy balance sheets, operators have little choice but to pass these costs onto the end consumer via higher tariffs.

Makes sense?

Reliance JIO IPO is round the corner as well.

26

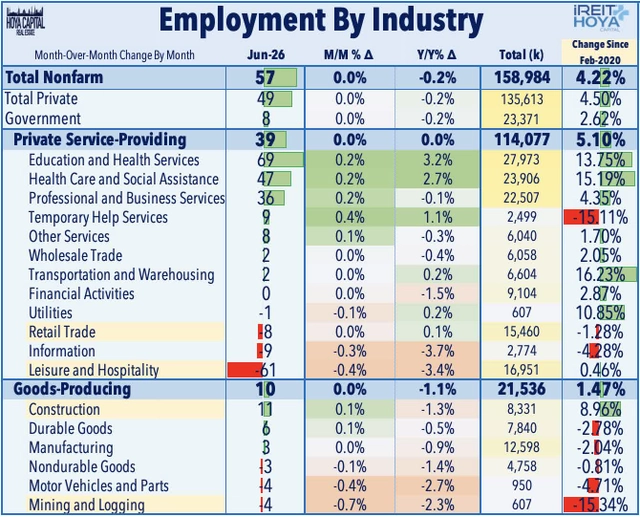

The industry-level details were mixed, with hiring increasingly concentrated in a narrow set of service categories while consumer-facing sectors showed renewed weakness. Education and Health Services remained the primary engine of job growth, adding 69k jobs in June, including 47k in Health Care and Social Assistance. Professional and Business Services added a solid 36k jobs, helped by a 9k rebound in Temporary Help Services - a modestly encouraging sign after a long stretch of weakness in that leading cyclical category. Goods-producing employment was also positive, adding 10k jobs, including 11k in Construction and 3k in Manufacturing, consistent with continued support from nonresidential construction, data-center demand, and defense- and infrastructure-related activity. The clear downside came from Leisure and Hospitality, which shed 61k jobs - its largest monthly decline since 2020 - as weaker-than-usual seasonal hiring overwhelmed expectations for a World Cup-related boost. Retail trade declined by 8k, Information fell by 9k, and Mining and Logging declined by 4k. Information employment has now remained one of the most persistent soft spots in the labor market, reflecting the ongoing restructuring across software, media, and internet companies as firms offset elevated AI investment and reposition their workforces.

1

1

Dear @winexviv,

I have an idea: EduChamp — a Southeast inter-school sports competition, structured like the Maths Olympiad, but for sports.

Schools compete across multiple sports. At the end, the best-performing students earn scholarships, and top schools win sports infrastructure upgrades.

The goal is twofold:

Motivate talented young athletes to take their education seriously — you can’t win for your school if you’re not in school.

Rebuild our grassroots sports system from the ground up, giving scouts a structured pipeline to discover talent early.

Education and sport shouldn’t compete for a child’s future. EduChamp makes them teammates.

What do you think?

Bhai itna bhi nhi h, Hm sab chahte hai ki 2 nosel lage ek E10 aur ek E20 bcoz har Petrol pump mashine 2 nosel wali mil jayegi.. 4-4 nosel lgane k liye pura infrastructure/ mashine new lgani pdegi , storage bhi 4 types ke alg alg bnane pdenge aur uske alawa ek diesel ka alg

1

Chetan Patil retweeted

THIS IS MINDBLOWING 🤯🔥

BJP built infrastructure is collapsing in six months and few even before inauguration

INC built this sea link in 2009

Even after 17 years, you can see there's 00 Potholes, 00 cracks and no jerkings 🔥

Just look at the quality of drive and this is what happens when you vote for development

152

633

2,956

173,409

Global News Brief — July 6, 2026

🌍 Geopolitics

Geopolitical tensions remain an important backdrop, but they are no longer the primary driver of markets.

Middle East: Oil markets remain relatively calm despite unresolved U.S.–Iran negotiations. Shipping through the Strait of Hormuz has remained steady, helping reduce fears of an immediate supply disruption.

NATO Summit: Leaders are gathering in Turkey this week, where defense spending, alliance priorities, and regional security are expected to dominate discussions. The summit could have implications for defense contractors, fiscal policy, and European security strategy.

Ukraine: Fighting continues, including Ukrainian drone strikes on Russian infrastructure, reinforcing that the conflict remains a persistent geopolitical risk even as markets are focused elsewhere.

📊 Macroeconomics

The macro narrative has shifted back toward growth, inflation, and central bank policy.

Key developments:

Last week's weaker-than-expected U.S. payroll report (57,000 jobs) reduced expectations for a near-term Federal Reserve rate hike.

Attention now turns to:

Federal Reserve meeting minutes (Wednesday)

ISM Services PMI

Speeches from several Fed officials throughout the week

Lower oil prices have also eased some inflation pressure, improving sentiment across equity markets.

For macro investors, this represents a transition from geopolitical-driven pricing back toward monetary policy and economic fundamentals.

📈 Financial Markets

Markets started the week on a constructive footing.

Equities

S&P 500 futures: 0.5%

Nasdaq futures: 1.1%

European equities remain near record highs.

The rally continues broadening beyond mega-cap AI stocks into industrials, healthcare, and financials.

Energy

A major development overnight:

OPEC announced another production increase of roughly 188,000 barrels/day beginning in August.

Brent crude fell toward $72/barrel, its lowest level in several months.

Lower energy prices reduce inflation pressure and generally improve global financial conditions if sustained.

Currency Markets

The Japanese yen remains one of the most closely watched macro risks. Continued weakness raises the possibility of intervention by Japanese authorities, with potential spillover effects into global bond and equity markets.

🤖 Technology & AI

The AI investment cycle remains intact, but investor scrutiny is increasing.

Today's themes include:

Semiconductor shares rebounded after last week's pullback.

The second-quarter earnings season begins this week, and AI-related guidance will likely be the most closely watched aspect of corporate reports.

Samsung Electronics is expected to report a sharp increase in profits, reflecting sustained demand for AI memory chips.

SK Hynix is proceeding with a large U.S. listing, highlighting continued investor appetite for AI infrastructure.

Meanwhile, the UN Global Dialogue on AI Governance begins today in Geneva, where governments and experts will discuss the opportunities and risks posed by advanced AI systems ahead of the launch of the AI for Good Global Commission.

💼 Business & Corporate Developments

Several notable business stories are developing:

Sky announced a £1.6 billion agreement to acquire ITV's broadcasting and streaming business, creating the UK's largest commercial broadcaster.

easyJet shares surged after agreeing in principle to a reported £5.5 billion takeover proposal.

Global M&A activity remains robust despite elevated interest rates, suggesting corporate confidence has held up better than many expected.

1

Unified Data: Sync the hub and the app.

@BCoreSolution, we turn these "oops" moments into high-stakes opportunities to build loyalty.

If your CX is leaking value, we should talk. Let’s build a better infrastructure.

#BuildInPublic #CXStrategy #BridgeCoreSolution

1

1

Thanks retweeted

They call them “data centers”.

But what they really mean is…

Deep inhale.

“What we’re building is the infrastructure for large-scale surveillance and a future where nearly everything is tracked, monitored, and confined to a digital system by 2030…”

Exhale.

109

557

1,851

25,062

Read the documents, not the headlines.

The DTCC is discussing:

• Tokenized capital markets

• Real-time settlement

• Interoperability

• DLT infrastructure

• @Ripple @coinbase & @circle competing in brokerage, exchange, custody and clearing (subject to regulatory approval)

The future won’t be one blockchain.

It’ll be an ecosystem.

dtcc.com/-/media/collateral-…

Sharmeen Mukhtar 🇵🇸 retweeted

I agree. No infrastructure in the world can handle such unprecedented levels of rainfall.

Except a bridge from 1830s.

The average rainfall numbers the Lonavala region (where the missing link is) for the ENTIRE month of July is around 700mm.

The same place received 670 mm of rain in 24 hours.

No infrastructure in the world can be planned for such extreme rain events. The rainfall numbers, if true, are absolutely mind boggling and would easily make it to the top 10 list of highest rainfall ever recorded during a 24 hour period in India.

That being said, ideally, the missing link should have been opened after undergoing the toughest litmus test on the planet that is the Indian monsoon.

77

798

6,131

174,010

That prediction market demo says a lot. Canopy makes sovereign chains feel less like heavy infrastructure and more like a builder tool. Lower friction is how more real developers enter Web3.