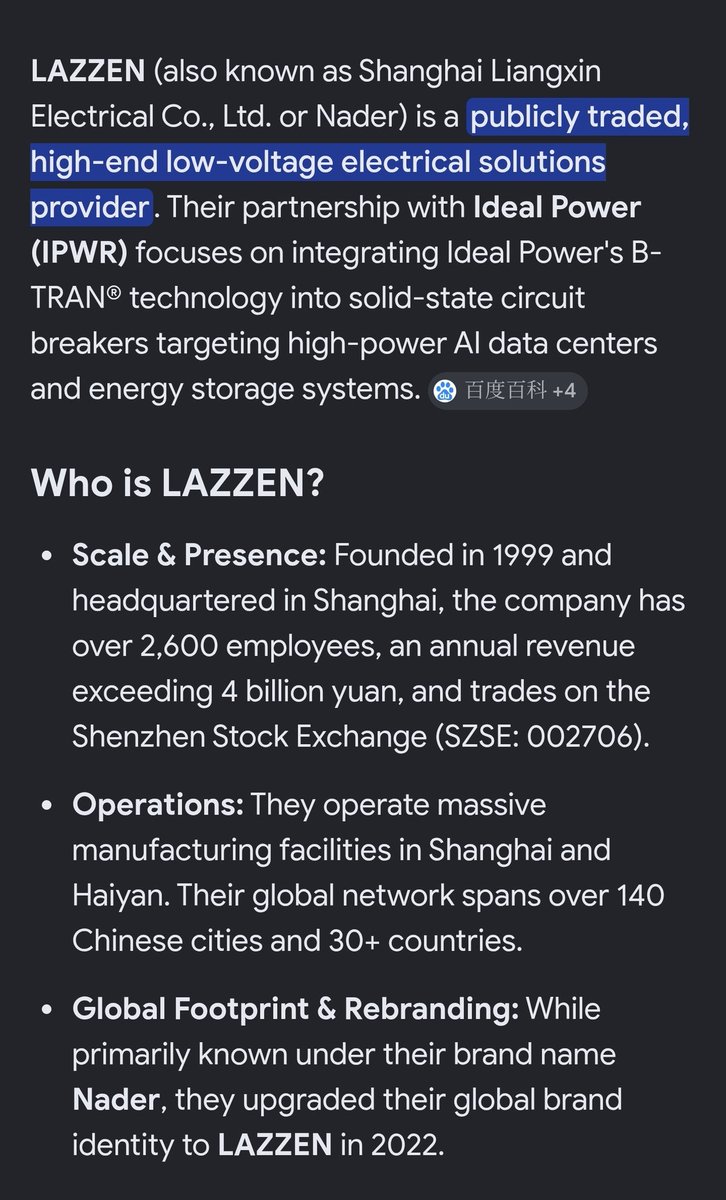

$IPWR There is a hidden chokepoint inside NVIDIA's Rubin Ultra rack that is being overlooked… remember this name B-TRAN

AI racks used to pull 10 to 50kW. Rubin Ultra is pushing toward 600kW and the roadmap points at megawatt racks. At that density, old 400V AC power delivery falls apart. Too much current, too much copper, too much heat. So the entire industry is ripping it out and moving to 800V DC.

800V DC fixes the power problem but creates a new one. DC current does not have a natural zero-crossing the way AC does. When a fault hits, the arc does not want to die. Mechanical breakers are way too slow to catch it. At 800V across a 120kW rack it is a fire.

So the rack now needs a new kind of breaker. Solid state. Reacts in microseconds. NVIDIA's own 800V reference architecture lists it as required infrastructure

This is where

$IPWR shines.

Think of a power switch as a gate on a road. Almost every gate only opens one way. If you need traffic flowing both directions, you bolt two gates together. Two gates means double the parts, double the cost, double the heat 🔥

$IPWR built a single gate that flows both ways on its own. They call it B-TRAN. One part instead of two. Traffic barely slows down so it runs cool. In its target jobs it wastes roughly a quarter of the energy a conventional setup does.

A safety breaker is the perfect fit. It sits open nearly 100% of the time and only slams shut when something breaks. When a part is on almost constantly, wasted energy is the entire ballgame. Run cooler, win the socket.

The demand is up there.

$WOLF just guided its data center power business to grow 30 to 50% per quarter. The 800V transition is happening now, not in 2030.

The execution is the bet.

On May 14

$IPWR signed an LOI to co-develop a B-TRAN solid state breaker prototype for a US hyperscaler building on NVIDIA's Rubin Ultra 800V architecture.

Prototype targeted for end of 2026, with a possible production ramp in 2027. Their pipeline grew about 50% since the start of the year. New CEO came from 11 years at

$ON, hired specifically to convert lab projects into real orders.

The not so rosy part:

$IPWR has $0 revenue today. No production orders yet. The whole thesis rests on one thing: turning a prototype eval into a repeating purchase order. Until it lands, this is a lottery ticket on B-TRAN becoming the default safety standard for 800V.

But it is a lottery ticket with a floor. No factories, no debt, $16M plus in cash after a recent raise, slow burn. It cannot implode the way

$WOLF did a couple years back. The downside is dead money, not zero.

This is a binary event with capped downside and uncapped upside. Still size accordingly to a pre revenue company.

This is the kind of name where if the design wins this explodes hard.

By the time there is coverage, the entry is gone. So I’m betting they win.

NFA. I hold a position in

$IPWR.