Next CPI could be the nail in the coffin for a much larger downturn in stonks.

Still too early to call for a market top, (though this is how I’m taking a jab at it) but once the top is in, I expect at least a 30% correction on

$nq and

$spx as the AI bubble gets crushed.

The NFP report yesterday confirmed that the Fed’s focus in the foreseeable future will be on inflation as the job market is much stronger than expected.

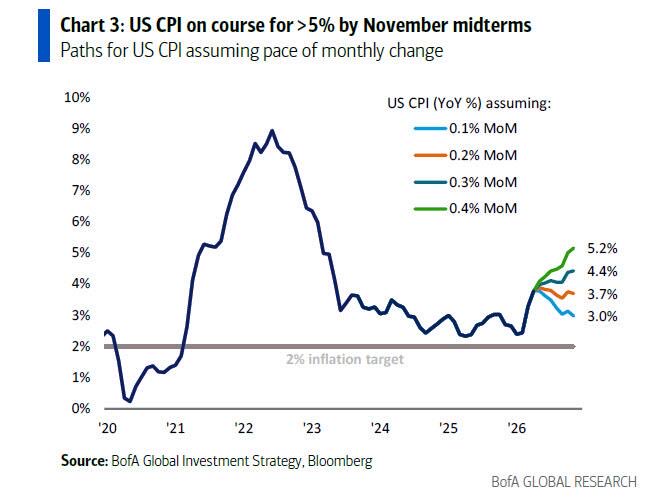

Inflation is running hot, we’ll know how hot June 10th.

« For now, Hammack said in a statement Friday, it is reasonable to hold rates steady. “But if recent trends continue, it may soon be appropriate to act,” she said, using language that suggests she is prepared to push for a rate increase as soon as the Fed’s subsequent meeting at the end of July. »

- WSJ

“But Pump inflation is good for risk assets”

In 2021, the Fed had 0% rates and $120B/month of QE because they chose to, carried by a disinflationary backdrop, and a reputation intact.

In 2026, they have 4% rates and $330B/year of QT because they have to, and reputation at risk under Warsh.

Complete opposite leeway. In 2021, easing was costless but today every option triggers a worse problem.

We just saw 3 hawkish dissents at the last FOMC. The most since 1992, with members arguing the statement language was too dovish.

Economists flag a 6-month average lag on energy passthroughs, and the Strait is still closed. Roll forward 4-6 months of 0.4% MoM CPI and you’re at 5.0% inflation by EOY.

The Fed’s reaction function from 2009-2021 (cut and ease at any sign of trouble) is no longer available without massive costs the market will price immediately on the long end.

All eyes on the next CPI print and the June FOMC.